By Peter Garnry

This year has seen some dramatic trends from the crunch in value stocks to the outrageous performance of stocks exposed to the green transformation and the digital economy. We discuss all the themes this year and whether they will continue in 2021 or whether we will experience turn of events with new powerful themes emerging.

This year has surpassed even our wildest imagination with a global pandemic racing the world causing severe restrictions crumbling economic activity on a scale not witnessed since World War II. Despite this horrible backdrop we have witnessed some extraordinary events in global equity markets from large winners and losers across companies, industries, and countries. We look at this year’s trends and whether they will continue next year.

This year’s winners and losers

If we look at the two biggest equity markets in the world, the US and Europe, then there is a clear signal across the winners and losers among single stocks. The 20 best performing stocks across these two markets have had an average return year-to-date of 148% in local currency as of last Friday driven by strong gains across stocks such as Etsy, Sinch, Hellofresh, NEL and Adyen all being part of the digital and green transformation trends this year.

The pandemic has lifted companies exposed to the digitalization and governments have increased their investment commitments on the green transformation with a new “green deal” in the EU lifting companies with exposure to green energy.

One company that is not on the list of winners is Tesla but would have been on the list if the company had been part of the S&P 500 Index. Tesla has become one of the most valuable companies in the world this year as demand for electric vehicles has grown dramatically despite the economic fallout fueling a multiple expansion discounting Tesla dominance in the future car industry and big player in the future of energy markets. Tesla was recently admitted into the S&P 500 index and the inclusion happens today.

Among the 20 worst performing stocks the average total return has been -54% this year in local currency driven by European stocks. On the losing list, we find European banks hit hard by the economic fallout, cruise lines and airliners hit hard by travel restrictions and then of course companies related to the oil and gas industry which have been hit hard by lower demand for energy.

The energy sector also delivered a true outlier in financial markets history with the first ever negative futures prices with WTI crude going negative as the market ran out of storage capacity. It was a short anomaly and the market quickly normalized again.

We know from the equity factor literature that performance over the past 12 months has a tendency on average to extend, this is also called the momentum effect, so based on past experience we should expect these trends in single stocks to continue, that is digital and green energy companies to continue higher and everything travel related to continue underperforming.

But we would argue that this year has been so special that this relationship has a high likelihood of not extending and thus we could see strong mean reversion effects in these performance lists. A better than expected vaccine roll-out is naturally a key necessity for this pattern.

Emerging markets have shown strength

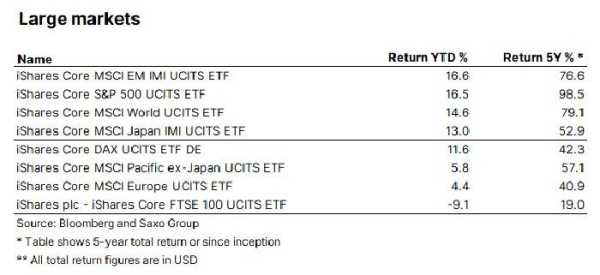

Based on closing prices on Friday, emerging markets had been the best performing market this year ahead of US equities reflecting the better relative handling of COVID-19 in Asia which has enabled the region to faster resume production capacity and exports goods into the developed worlds, but also seeing a faster rebound in consumer confidence and spending.

The positive rebound in Asia causing emerging market equities to hit a new all-time high in US dollar has also spilled into Japanese equities up 13% year-to-date.

Europe has once again been a weak market driven by poor handling of the COVID-19 pandemic, Brexit tensions that could end in a new no-deal deadline extension on Dec. 31 if the UK and Europe cannot agree on a trade deal.

European equities have become one of the cheapest equity markets in the world and in theory a hunting ground for value investors, but the continent’s equities are cheap for a reason. It lacks a big publicly listed technology sector, and the economic engine is impaired relative to other parts of the world. Maybe the green transformation and related stimulus will revert the ugly trends for Europe in 2021.

The value crunch and the disbelief in ‘quants’

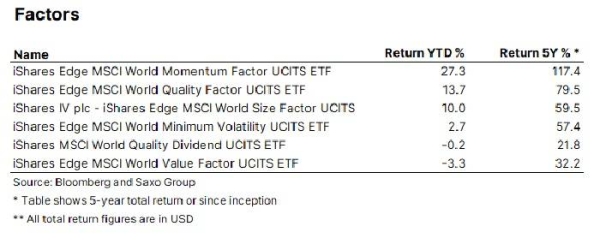

Looking across equity factors the overshining story this year has been the absolute crunch of value stocks which are heavily tilted towards financials, miners, energy, utilities and industrials which have all been hit hard by the COVID-19 pandemic. To sum it up in short, cheap stocks have become cheaper and expensive stocks have become more expensive leading to some of the world’s largest quant funds to write many papers explaining the value crunch and that now is a better time than ever to bet on cheap stocks.

It might be true, but it likely depends on a few things such as higher interest rates and inflation, and retail investors losing their appetite in equity markets. Recently many investors have talked about the “great value rotation”, but while we recognize the potential, we are not onboard yet. We need to see a breakout of interest rates combined with higher inflation before we join the crowd, and with today’s move due to the new COVID-19 mutation in the UK the value rotation might take a bit longer than expected.

The fall of value stocks this year has many similarities to the 1998-2000 run-up in equity markets and in particularly technology stocks. The retail participation is high again, and estimated to be around 20% of equity flow in the US by some US market makers, but amplified this time by a significantly larger among of call options on top of the cash equity activities forcing market makers in options to push up the underlying stocks through their hedging activities.

Retail investors do not invest, or trade based on sophisticated valuation models but invest instead on stories and simple technical momentum indicators. These forces amplify momentum trades and push up already expensive stocks because they are also the ones showing up on momentum indicators. A forceful feedback loop is in play.

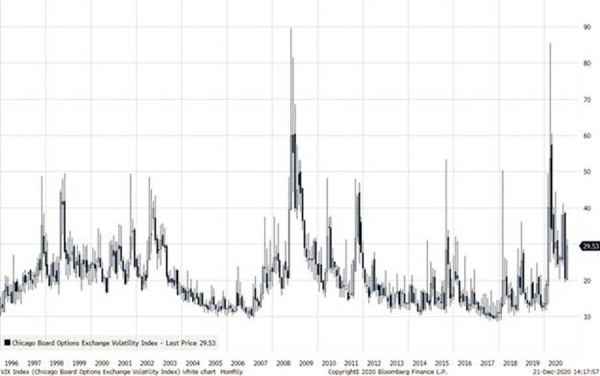

Another striking similarity to the dot-com days is the elevated VIX Index together with the strong momentum. In the years 1998-2000, the VIX Index was hovering around 25 on average something the short volatility traders of the past seven years would have a hard time comprehend as the VIX Index has rarely been above in 20 in a sustained manner until 2020 where it has only briefly dipped below 20.

As some quant funds suffered in the years 1998-2000, at least those that heavily incorporated the value factor, some of the most well-respected quant funds have also had a hard time this year causing both investors and some well-known quant researchers to doubt the discipline itself. This could be a sign that we are reaching some inflection point, but we do not really know as crazy periods can go on for a long time. But one thing is for sure, we have had a structural shift in the market this year because hedge funds such as Renaissance Technologies are not stupid and if they have been wrongfooted this year on their longer term signals/factors then something profound happened.

Online vs offline

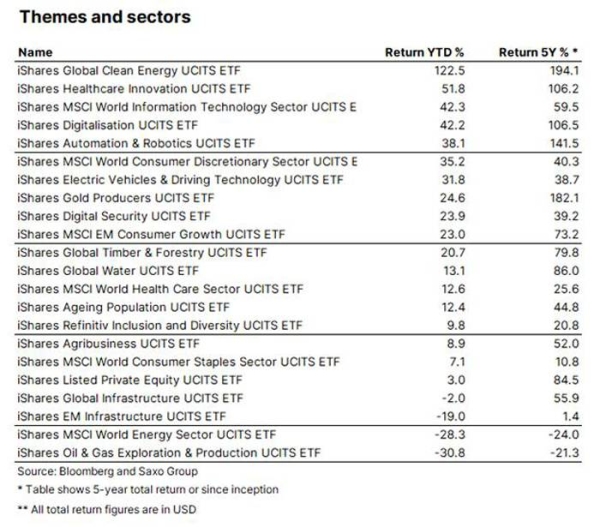

This year will be remembered for the spectacular rebound and returns in stocks related to the online world and the green transformation. As the table below shows, the big winner has been clean energy stocks up 123% year-to-date as investors are betting that the new Biden administration in the US will massively change the landscape for clean energy stocks in the US.

China has recently committed itself to become carbon neutral before 2060 and is thus expected to dramatically shift it investments over the coming 10 years. In Europe, which was already leading the game the recent “green deal” will just turbocharge this trend. As we wrote in early January, the green transformation will most likely be one of the biggest trends in financial markets over the coming decade and some of the world’s most valuable companies in the future will be those that help solve the problems related to our environment and climate change.

The three other wining themes this year have been companies in health care and especially those involved in COVID-19 tests and vaccines, but in general the entire sector has been lifted, and then of course digital companies within delivery services, e-commerce and software including work-from-home stocks.

Finally, the automation and robotics theme has seen a boost as investors are betting on more automation as a result of COVID-19 as robots are immune to viruses and thus the more we automate the less fragile our production and supply chains become to future pandemics.

The flipside of the rise of stocks with exposure to the digital economy is the physical world. The losing themes this year have been energy, infrastructure, and private equity. However, the latest signs of rapidly rising shipping rates and logistics costs and higher commodity prices, we are beginning to see the inflection point of a physical world that has reached a temporary limit on its ability to support the demand coming the digital economy.

The latest news from Apple expecting a 30% increase in iPhone production is said to have difficulties sourcing enough components to meet the demand. The long winning streak of the digital economy in the past 10 years have caused an underinvestment in the physical world to a degree where the physical world will need higher prices to send out signals to investors in order to get investments and expand supply.

What to expect in 2021?

Forecasting is a fool’s errand but nevertheless we will try to formulate our best guesses on what to expect in 2021. Our core argument is that policy makers will make the policy mistake of overstimulating the economy on top of a better than expected vaccine rollout. This will cause the economy to run hot next year pushing up real inflation in the physical world and with that long-term interest rates and thus significantly steepening the yield curve.

This will help financials and companies exposed to the physical world and thus value stocks could have one of its best years ever. But will it create a plunge in technology stocks? If the interest rate rise is well behaved, and the US 10-year yield stays below 2% then our guess is that technology stocks will continue to rise but lose out to value stocks on a relative basis.

If we move beyond 2% on long-term yields, then the rate sensitive stocks (the super aggressively priced growth stocks) could experience a seismic change in valuation and a dramatic collapse in their stock prices. This move will most likely be linked to Europe, which may have a good year in equities for once.

The US-China tension will continue to rise next year, and supply chains will continue to change with more companies diversifying their production out of China. This will add to the rise in inflation as globalization over the past 40 years with China turning into the world’s factory has put a lid on prices.

But despite of these changes the emerging markets will continue to do well, and we believe this part of the equity market will do very well next year. Green energy can almost only disappoint as the sector is priced for perfection, but momentum trades can continue much longer than what would seem rational.

Next year could also be the year when investors are scared about the willingness of governments to intervene in markets to restore competition, especially in the digital economy. The trajectory is for regulation and the big potential headline next year could be that of breaking up Facebook or forcing Google to “open up” technology in search and other related technologies so competition can increase.

We saw similar moves in the 1960s with IBM and AT&T/Bell Labs, so it could happen again. Amazon is ripe for an antitrust move by the US government but our guess is that Amazon will make a pre-emptive move by spinning out Amazon Web Services driven by the valuation that Snowflake just recently got in its IPO but also because it can divert attention for a while.

One thing is for sure. Only half of the above guesses will come true and something crazy will likely hit the world that makes these forecasts look stupid in hindsight when the calendar reads December 2021. But we feel confident that next year will throw new dramatic moves at investors, unless this is our ultimate failed prediction and markets become unusual quiet next year with super low volatility again. Time will tell.

— The writer is head of equity strategy at Saxo Bank