DUBAI — After a material improvement in growth and earnings in 2019, S&P Global Ratings expects the Saudi Arabian insurance sector to report solid underwriting results in first-half 2020, benefiting from fewer motor and medical claims due to the COVID-19-related lockdown, despite negative economic growth.

We now forecast Saudi economic output (measured in GDP) will contract by about 3% in 2020 before we see modest positive growth of 1.6% in 2021. As the effects of COVID-19 and lower oil prices evolve, we will update our economic assumptions and estimates accordingly.

With the lifting of strict lockdown measures in late June, we expect that motor and medical claims will pick up, as traffic flow increases and policyholders start returning to hospitals for non-urgent medical services in the coming months. The increase in value-added tax (VAT) to 15% from 5% from July 1 and cuts in social benefits for citizens could further pressure consumer spending, in our view.

Insurers are therefore likely to experience a slowdown in premium collections, since many consumers and businesses could delay their premium payments in an attempt to manage cash flows. This would pressure asset quality, liquidity, and consequently credit conditions of some players.

However, we expect the sector to still remain profitable overall in 2020, despite slower premium growth and substantially weaker profitability in the second half. Following two recent merger announcements, we expect to see further and accelerated consolidation in the sector over the coming quarters, given that there is a relatively large number of small and loss-making insurers.

Better Underwriting Results Are A Key Profitability Driver

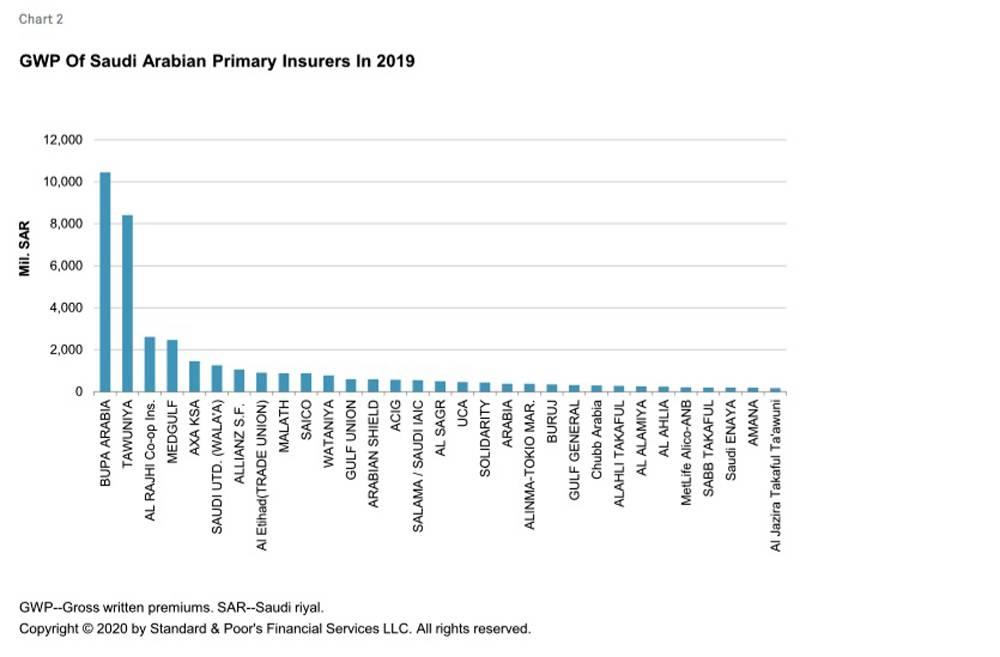

Following two years of declining gross written premiums (GWPs), the Saudi Arabian insurance sector saw GWP growth of about 8.3% to SR37.8 billion in 2019 from SR34.9 billion in 2018.

This was mainly spurred by rate increases and the extension of mandatory medical cover to a wider part of the population, as some previously loss-making insurers successfully repriced their policies.

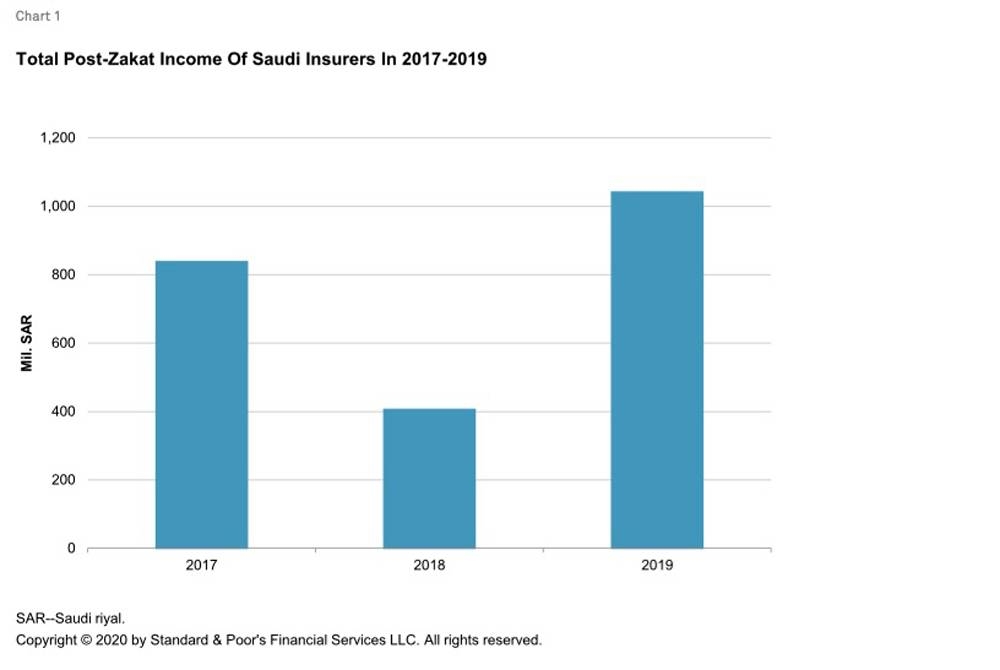

At the same time, post-zakat (religious tax) income increased significantly, by about 146% to about SR1 billion in 2019 from SR406 million in 2018 (see chart 1). This was mainly due to stronger earnings at some leading insurers including Tawuniya, BUPA Arabia, and MedGulf.

Insurers Could Be Negatively Affected

Measures taken to contain COVID-19, including travel bans and curfews; lower oil prices, leading to delays or cancelations of nonessential infrastructure projects; and a general decline in disposable income due to the VAT increase and social benefit cuts could negatively affect GWP growth and earnings prospects over the next year.

We anticipate that the number of insured individuals under medical policies will decline and that some employers will opt for more basic and cheaper medical cover for staff in an effort to save costs. A slowdown in economic activity and consolidation in a number of sectors has already led to job cuts and cost-saving measures in recent years.

Although the local population continues to expand, this will likely be offset by the departure at least 600,000 (mainly blue-collar) foreign workers that could be forced to leave Saudi Arabia in 2020 due to job losses or Saudization requirements. In addition, consumers will also likely defer purchases of new cars and other items due to economic uncertainty.

Although the introduction of new mandatory medical cover and an effort by the authorities to reduce the number of uninsured cars (currently, only about 50% of cars in Saudi Arabia are adequately insured), will lead to satisfactory growth in the medium term, we now anticipate that total GWP will decline by up to 5% in 2020.

In our view, new mandatory medical covers for Hajj and Umrah pilgrims that were introduced in early 2020, but put on hold due to COVID-19-related travel restrictions, could generate additional GWP of SR1.5 billion-SR2.5 billion in 2021 and help the market return to growth.

However, this is assuming foreign visitors are allowed to attend the pilgrimages next year. We also believe long-term life insurance products, which currently contribute less than 4% of total GWP, may experience an increase in demand, particularly for coverage of critical illnesses.

We understand that the Saudi government has agreed to cover the majority of medical care costs related to COVID-19 and that claims relating to non-urgent medical treatment substantially declined in first-half 2020. In addition, strict lockdown measures also led to a material decline in motor claims during that time.

We expect that most insurers will report favorable underwriting results in first-half 2020. However, with the lifting of lockdown measures in late June, we expect that motor and medical claims will return to more normal or slightly elevated levels in the coming months, as traffic flow increases and policyholders start visiting hospitals for non-urgent medical treatment.

In addition, insurers have agreed to extend motor policies for two months free of charge, which will broadly offset the decline in claims during the lockdown.

Another key issue for insurers this year will be the VAT increase to 15% on July 1. When a 5% VAT rate was introduced in January 2018, insurers had to cover a substantial part of the tax burden because they were unable to fully recover VAT for policies written in 2017 that extended into 2018. However, we expect the VAT increase this year will have a modest effect on profitability because the General Authority of Zakat and Tax (GAZT) has issued guidance suggesting that the higher rate will not be applicable to policies issued prior to May 11, 2020.

Despite this transitional period, insurers might have some additional tax liability for annual policies written between May 11 and July 1. We estimate that this additional tax liability could be up to SR300 million for the whole market over 2020 and 2021.

Although we understand that insurers are permitted to invoice policyholders or offset the additional VAT costs when paying claims, these liabilities may still not be fully recovered.

More broadly, we think profitability could be affected by a likely slowdown in premium collections, since many consumers and businesses could delay their premium payments in an attempt to manage cash flows. Under existing regulations, insurers in Saudi Arabia are required to fully provision for receivables that are outstanding for more than 90 days, which typically has a negative effect on solvency buffers.

In anticipation of longer payment cycles, we understand the regulator has granted insurers permission to treat receivable that are outstanding for more than 90 days more favorably--similar to practices in other markets--to ease potential pressures on solvency calculations.

Meanwhile, on the asset side, the sector has limited exposure to risky asset classes such as equity and real estate, which together contribute to less 20% of total investments. However, the equity market (Tadawul) has declined by about 13% in the year to date (June 28).

This decline, in combination with lower interest rates, will likely lead to lower investment returns in 2020 than in 2019. Overall we believe that profitability will decline in 2020 and fall below 2019 levels, when the sector generated a post-zakat profit of about SR1 billion.

Overall Capitalization Remains Satisfactory, But Weak Earnings Will Lead To Further Consolidation

The sector's total shareholder equity increased by about 10% to SR16.4 billion in 2019 from SR14.9 billion in 2018, since a number of insurers retained profits or raised additional capital through rights issues. Like the previous year, growth in shareholder equity exceeded premiums in 2019, which indicates a slight improvement in overall capitalization.

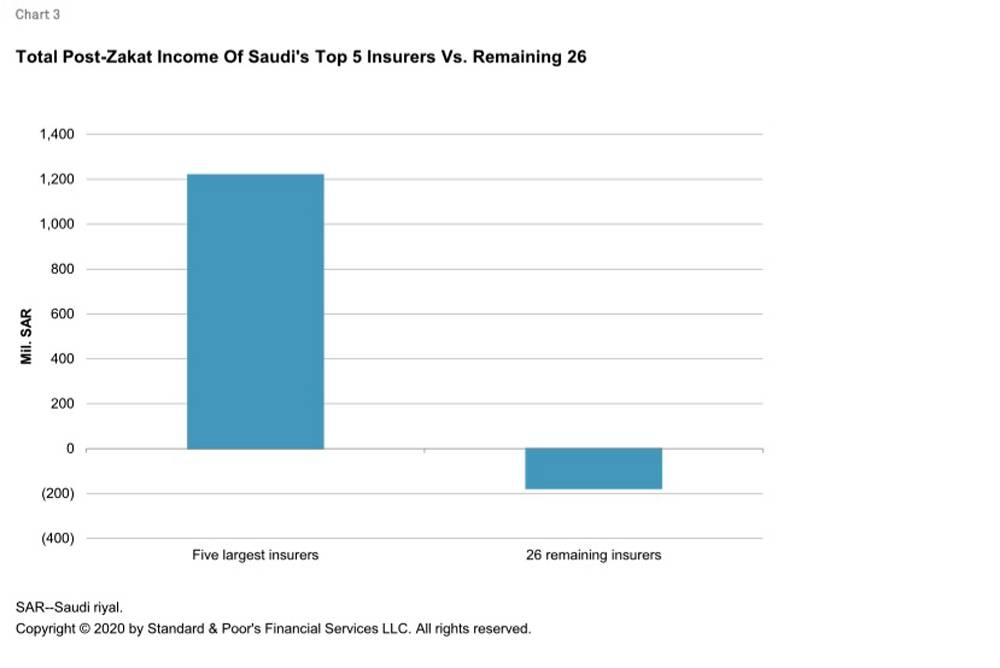

However, Saudi Arabia's insurance sector remains highly concentrated in terms of GWP and earnings. In 2019, the five largest primary insurers (out of a total of 32) had a market share of about 68% (2018: about 66%). Moreover, the largest insurer, BUPA Arabia, crossed the SR10 billion GWP mark for the first time, but there were 13 companies that generated less than SR367 million ($100 million) and another six that wrote less than $200 million.

There were also differing fortunes across the market, with the five largest insurers by GWP reporting a combined post-zakat profit of about SR1.2 billion in 2019 and the remaining 26 primary insurers a combined post-zakat loss of about SR177 million.

As in 2018, post-zakat losses were also reported by 13 insurers, representing about 42% of all primary insurers in the market. These companies had a combined market share of about 12%. We therefore believe that credit conditions for these small and loss-making insurers will continue to weaken, while they will remain broadly stable for the market leading players.

Although scale is no guarantee of profitability, it does help insurers to dilute some of their expenses, which are relatively high in Saudi Arabia compared with other markets. We note that three of the 34 insurers have stopped writing business in recent years due to insufficient solvency capital.

Following two recent merger announcements, we expect to see further consolidation through mergers or market exits in 2020 and 2021. However, given the relatively large number of loss-making players in the market, mergers will only be beneficial if shareholder expectations are realistic in terms of valuations and companies can benefit from factors such as larger scale, access to new lines of business, or other forms of diversification. — S&P Global Ratings