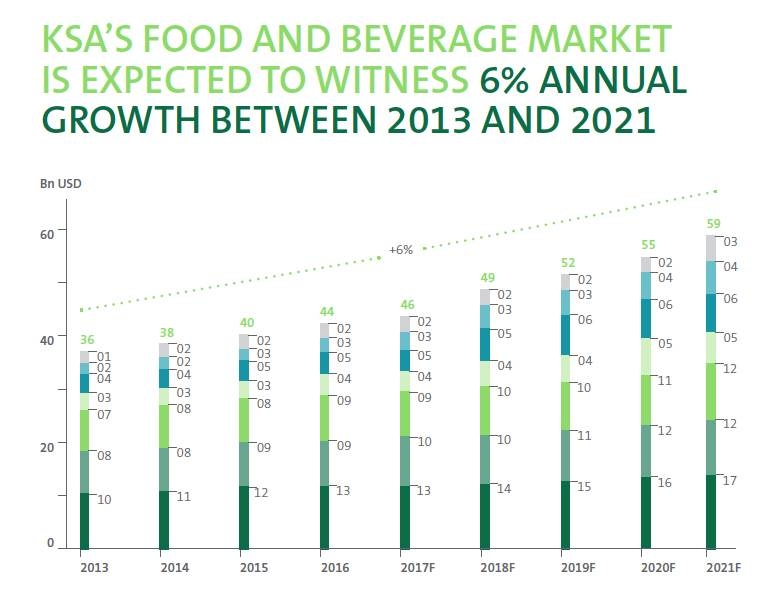

JEDDAH — The Saudi Food and Retail sectors are expected to yield good results in the third quarter of this year, Al Rajhi Capital Research said on its comments on Saudi Arabian equities, due to improving consumer spending and promotional activities.

Moreover, “we expect an improvement in like-for-like growth for most of the retail and food-based companies.

Telecom companies are expected to witness improved performance as we saw a mid-single digit increase in Haj pilgrims and newer packages introduced which could increase ARPUs. The downside factor is possible decline in expats in Q3. In the first two months of Q3, “we noticed a 6% y-o-y increase as compared to a decline of 5% y-o-y during the first eight months of 2019.“

Cement realizations are up 30% since the end of 2018.

In the petrochemical sector, Al Rajhi expects aggregate earnings of the Saudi petrochemical sector to weaken sequentially in Q3, mainly due to lower product prices and impact from lower feedstock supply from Abqaiq attacks. Average Brent crude price declined by c10% post weak demand concerns though it picked up in the later stages of Q3 due to the Abqaiq attacks. Overall as Brent declined, Naphtha, Propane and Butane prices declined by 10%, 24% and 27% q-o-q respectively. As these contribute on an average 30-35% of top-line, one could broadly expect the decline in feedstock prices to offset product prices decline for a large part, depending on product and feedstock mix. Among the companies under our coverage, we expect SAFCO is likely to see a sequential increase in net profit. For SAFCO the production volumes are expected to increase post the reliability enhancement project and for Sipchem we expect the full combined quarterly earnings to be reported in Q3 after the merger. Among the products, Urea, Polypropylene and MTBE products were among the relatively better performers in Q3 in terms of price. Market consensus expects an improved outlook for prices only by mid-2020.

In the banking sector, SAMA data indicated that banking sector profits rose 10.3% y-o-y and stood at SAR4,575mn in August. Banking sector credit to the private sector rose for the 17th consecutive month by 2.8% y-o-y (+0.3% m-o-m) and deposits grew by 5.0% y-o-y in August. This shows that so far performance of the banking sector

is healthy and going as expected. However, the caveat is that the provisions are taken usually in the last month of the quarter. Post the Fed interest rate cut on 18th September the market expects a weakness in NIMs. In Q2 NIM decreased marginally (4bps q-o-q) as SAIBOR came under pressure and continued to go down with expectations of cut in Fed rates. Al Rajhi Capita do not expect an immediate material Q3 impact because historically NIMs move at a slower pace as compared to SAIBOR especially for retail banks. Mortgage market is also expected to continue growing at a higher pace and boost EPS. Moreover, with government support mortgage loans have almost nil NPAs which could assist banks to report stable cost of risk. Moreover, in Q2 the asset quality deteriorated marginally and gross NPL ratio increased to 1.90% from 1.85% in Q1.

In the retail sector, Retail sector

“We are expecting a recovery in the overall retail sector compared to Q3 2018, we believe that the negative impact of VAT is past now and consumer spending has improved. We have observed a gradual recovery in LFL growth from Q4 2018 and we expect the LFL to turn positive for all the retail companies in our coverage. Sequentially we expect the overall profit of the retail sector to improve.” — SG