JEDDAH/DUBAI — Global Islamic financing increased by 14.6% to $32.95 billion in 2018 compared to 2017, Bloomberg said in its EMEA Capital Markets Tables, representing the top arrangers, bookrunners and advisors across various deals including syndicated loans, bonds, equity and M&A transactions in 2018.

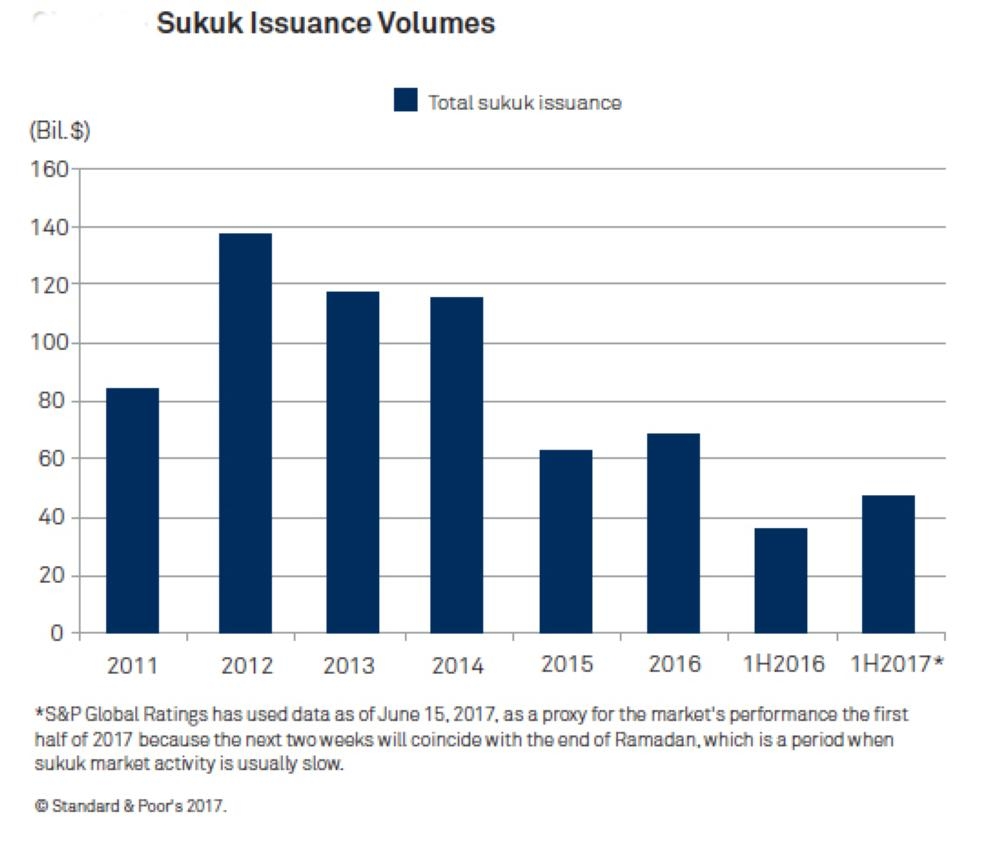

The report said Dubai Islamic Bank is the top bookrunner with 9.55% of credited market share. International sukuk credited volumes decreased by 14.2% to $25.06 billion compared to 2017. HSBC held the top underwriter spot with 13.54% of market share.

Bloomberg further said in the Middle East and North Africa (MENA) region’s syndicated loans, total MENA borrower loans increased by 52.8% to $127.2 billion compared to 2017. This is the highest amount on record, surpassing the previous high set in 2007. First Abu Dhabi Bank ranked as the top MENA borrower loans bookrunner for FY 2018 with 8.85% of credited market share. HSBC and Standard Chartered ranked second and third with 7.16% and 6.91% of credited market share, respectively.

Saudi Arabian-based borrower’s leads the rankings with 35.54% market share, followed by UAE and Oman -based borrowers with 27.61% and 9.9% respectively.

In bonds and sukuk, total MENA credited volume decreased by 12.8% to $86.5 billion, compared to 2017. This is the second highest amount on record, with the highest recorded in 2017.

Standard Chartered Bank ranked as the top MENA bonds and sukuk underwriter for FY 2018 with a market share of 16.46%. HSBC and Citi ranked second and third, respectively, with a market share of 9.84% and 8.27%. UAE-based issuers led with 25.34% market share, followed by Qatar and Saudi Arabia-based issuers with 23.35% and 19.87%, respectively.

Bloomberg’s league tables are a one-stop shop for constant and timely access to the most comprehensive information available on capital markets representation.

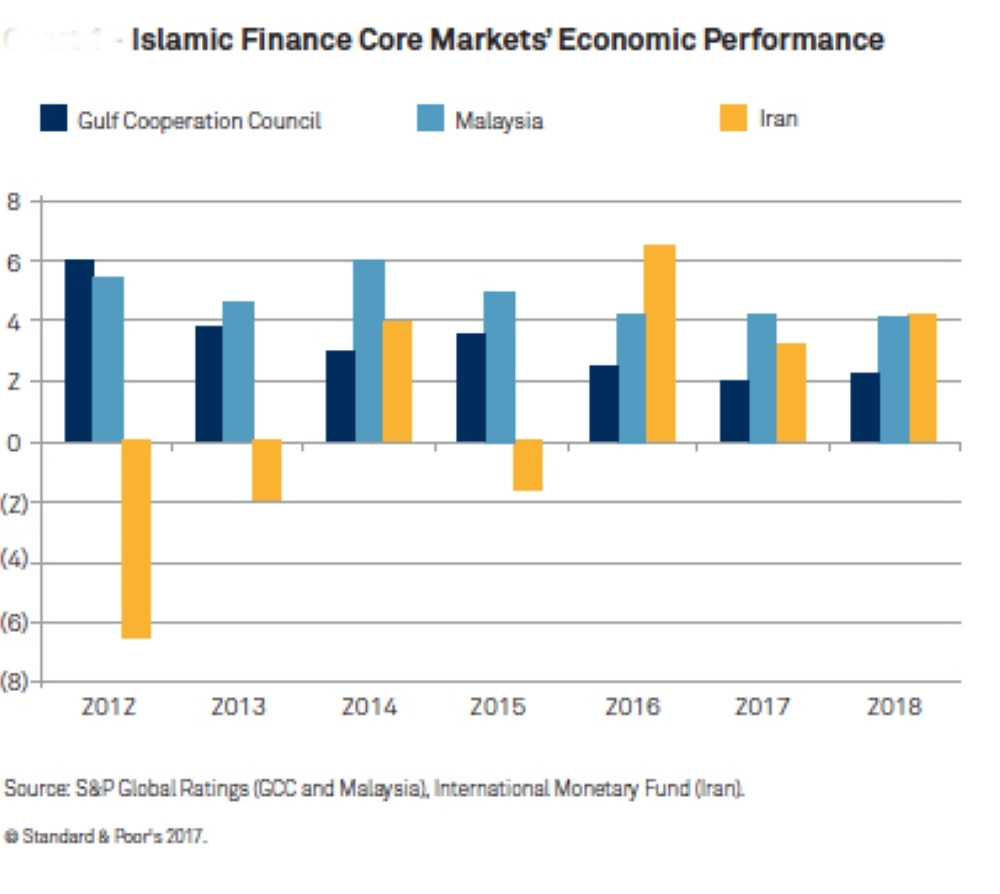

Meanwhile, S&P Global Ratings said in a separate report that Islamic finance remains concentrated

primarily in oil-exporting countries, with the Gulf Cooperation Council (GCC), Malaysia, and Iran accounting for more than 80% of the industry’s assets. The drop in oil prices and governments’ cuts to investment and current spending have reduced the industry’s growth prospects, S&P said. While Malaysia’s economy continued to perform adequately, thanks to its diversification, the average growth rate in the GCC dropped significantly between 2012 and 2017. Iran, on the other hand, experienced a growth spurt in 2016 after certain sanctions were lifted and the oil sector picked up, but this growth is expected to moderate over the next three years. Meanwhile, Iran’s economy will continue to suffer from the scarcity of financing options and the remaining sanctions.

Another factor explaining the muted industry growth is depreciation/devaluation of currencies in some countries. In particular, “we’ve observed a marked impact of this on Islamic finance activity in Iran, Malaysia, Turkey, and Egypt, where exchange rates have deteriorated.”

As the US dollar continues to strengthen in 2017 and 2018, S&P might see more of this effect. In this context, the Islamic finance industry was protected by the peg between the dollar and various GCC currencies.

“Overall, we think the industry’s growth rate will stabilize at about 5% in 2017 and 2018, which is lower than the average over the past decade (see chart 3). More recent industry entrants, such as Morocco and Oman, will likely show stronger growth, but their contribution to the overall Islamic finance industry will likely remain small.”

The report expect the slowdown at Islamic banks in the GCC will persist in 2017 after asset growth declined to 5.3% in 2016 from 10.7% in 2014. “In our base-case scenario, we assume that asset growth will stabilize at about 5% as governments’ spending cuts and revenue-boosting initiatives, such as new taxes, reduce Islamic banks’ growth opportunities in the corporate and retail sectors.”

“We see banks becoming more cautious and selective in their lending activities, triggering stiffer competition. Yet we don’t expect this will happen uniformly in all GCC countries.

Despite the United Arab Emirates (UAE)’s tepid economic performance and the drop in real estate prices, Islamic banks continued to expand by high single digits.

As the economic cycle turns, we think GCC Islamic banks’ asset quality indicators will deteriorate in the second half of this year and in 2018. Such weakening was not noticeable in 2016 because –as is typical –banks had started to restructure their exposures to adapt to the shift in the economic environment. Therefore we saw an increase in restructured loans in the GCC last year, but not a marked increase in banks’ nonperforming loans (NPLs) or cost of risk. “We think the deterioration will be more visible in 2017 and 2018. Overall, we believe that subcontractors, SMEs, and expatriate retail exposures will bear the brunt of the turning economic cycle and contribute prominently to the formation of new NPLs over that period.”

The cost of funding has increased, and this squeezed banks’ intermediation margins in 2016. Although the pressure eased a bit after some governments issued international bonds and unlocked payments to contractors, we think the cost of funding will remain inflated in 2017-2018. The U.S. Federal Reserve (Fed)’s recent rate hike, which some GCC central banks have emulated, could result in deposits shifting to profit-sharing investment accounts (PSIAs) from unremunerated current accounts. If this happens, it would raise the cost of funding even further. Very few Islamic banks have set aside significant amounts of profit-equalization reserves, which they build in good years and use to smooth returns to PSIA holders if needed.

- Cost of risk is on the rise. We also foresee higher credit losses in the coming two years, due to relatively weak economic conditions. Exposure to subcontractors, SMEs, and retail customers (especially expatriates) will likely fuel the upward trend for credit losses.

In general therefore, we expect Islamic banks’ revenue growth will decelerate, and that they will focus on their cost bases to mitigate the impact (for example, by pruning branches). Like their conventional counterparts, GCC Islamic banks, through their relatively low cost bases, should be able to protect their profitability somewhat over the next two years, however.

positive factor for GCC Islamic banks. We note, however, that it has reduced because previous rapid financing growth was not matched by additional capital. Few GCC banks have issued capital-boosting sukuk and those that have, are primarily in the UAE, Qatar, and Saudi Arabia, S&P Global Ratings said. — SG