DUBAI — Energy leads the way in 2018. Needless to say, 2018 does not have much in common with 2017. Back in 2017, energy was among the three worst performing sectors in Europe (+6.2%), after telecom services (+2.2%) and health care (+3.5%), and trailing far behind the best performers, i.e. information technology (+20%) and materials (+18.9%), according to Indosuez Wealth Management’s Equity Pulse.

In true contrarian fashion, the energy sector has been by far the best performing sector in Europe in 2018, — the sector is up 17.4% as of 22 May 2018, against 4.1% for the Stoxx Europe 600 Index. The sector represents 7% and 7.2% of today’s Stoxx Europe 600 Index and Euro Stoxx 50 Index, similar to the weighting of the energy sector in the US (6.4% of the S&P 500 Index). Furthermore, integrated oil and gas companies, which tend to be the largest companies, make up most of the total capitalization of the sector.

In our view, oil prices are to remain a positive driver for energy stocks’ performance. Companies in the sector have indeed already benefitted from the recent uptick in the price of Brent, from a low of $44.82/Bbl on June 21, 2017, to a new high of $79.57/Bbl on May 22. The recent acceleration in oil prices can be explained by rising concerns over supply including the decision by the United States to step out of the nuclear deal with Iran and to reintroduce economic sanctions. Our house view considers the supply and demand fundamentals supportive, as well as the geopolitics, given the tensions in the Middle East.

So far, in Europe, companies that have more exposure to upstream activities (exploration and production – E&P) have outperformed companies providing services and equipment to the petroleum E&P industry (i.e. downstream activities).

However, the increase in capital expenditure (capex) from global oil majors should be very supportive for companies providing services and equipment to the sector over the course of 2018.

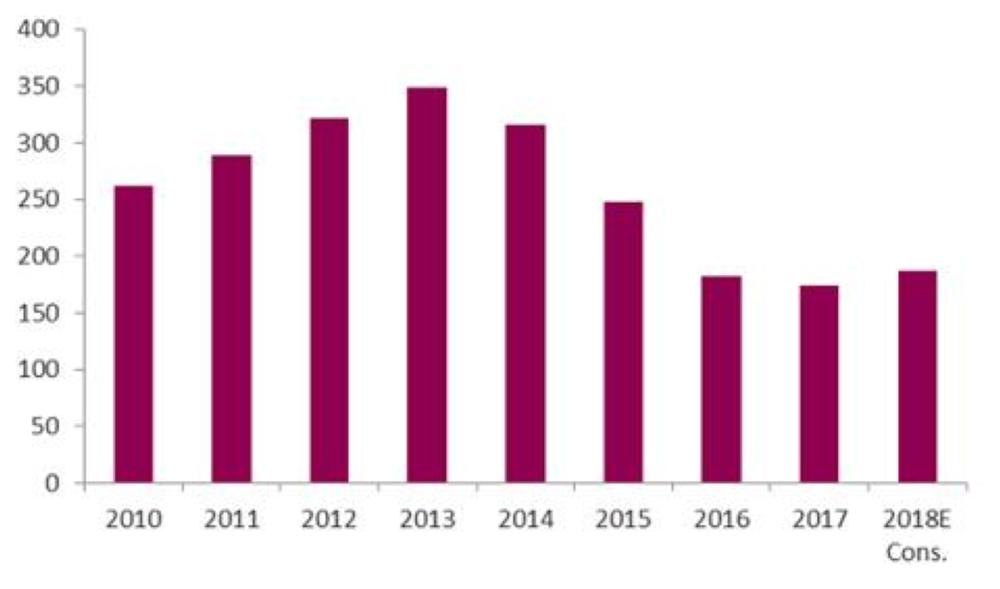

Indeed, the latter tend to lag the former when oil prices rise, since oil services and equipment companies depend on capacity improvement and expansion from companies that are active in upstream activities. The idea is very intuitive — companies increase their production capacities when they know that they can sell their product at a favorable price. In this regard, 2017 marked a turning point with global E&P capex up by 8% after an approximate 40% decline since 2014, according to Kepler Cheuvreux.

With regards to global integrated oil & gas companies’ capex, we find that spending was flat last year, but is expected to increase in 2018 for the first time in five years. — SG